From Shutdown to Renaissance

How America Fell Out of Love With Nuclear — and Fell Back In

The story of how the world’s most ambitious energy technology went from national disgrace to national priority in a single generation — and why the decade ahead will determine whether it stays that way.

This story is covering: The collapse after Three Mile Island | Four decades of regulatory paralysis | The regulatory revolution of 2026 (Parts 53, 57, and the fusion framework) | Trump’s deregulation and its double-edged consequences | The commercial explosion: Gates, Google, Microsoft, Amazon | Fusion energy: promise and timeline | AMPERA and the shipping-container reactor | What it all means

There is a serious demand for more power, to fuel the growth of data centers - an industry that, without nuclear, will still invest $5 trillion dollars in the next 3-5 years - outpacing the next 10 industry sectors in investment.

This is a long story, so feel free to skip around. There are details in here that AI did help me gather, but the motivation for this came while I was at Data Center World, where talk of nuclear or fusion (its little brother) was not uncommon.

TL:DR

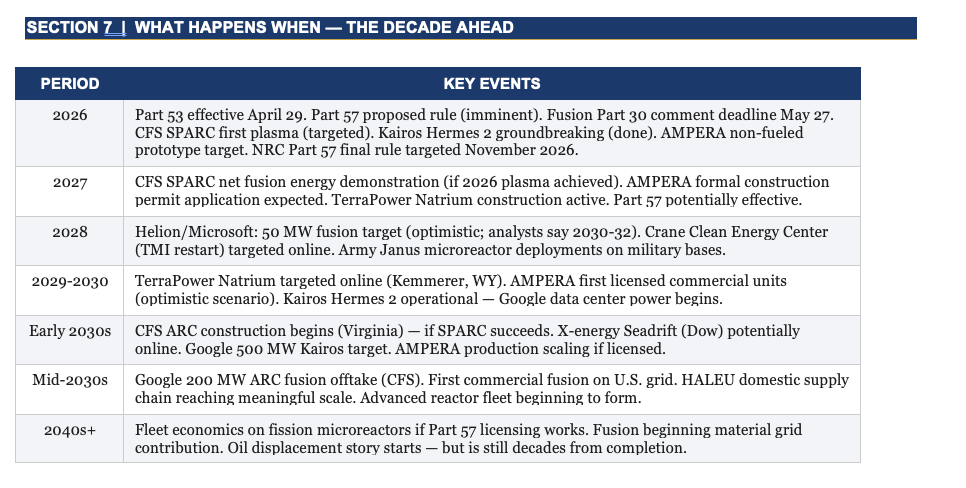

The NRC just rewrote its rulebook for the first time since Eisenhower. Part 53 is now law. Part 57 — a dedicated pathway for factory-built microreactors — is weeks away. A third rule opens commercial fusion to fast-track licensing for the first time in history. The game board is genuinely different.

Google, Microsoft, and Amazon aren’t buying nuclear power because they believe in clean energy. They’re buying it because AI data centers run 24/7 and solar doesn’t. Those signed contracts — and the capital behind them — replaced 40 years of utility hesitancy overnight.

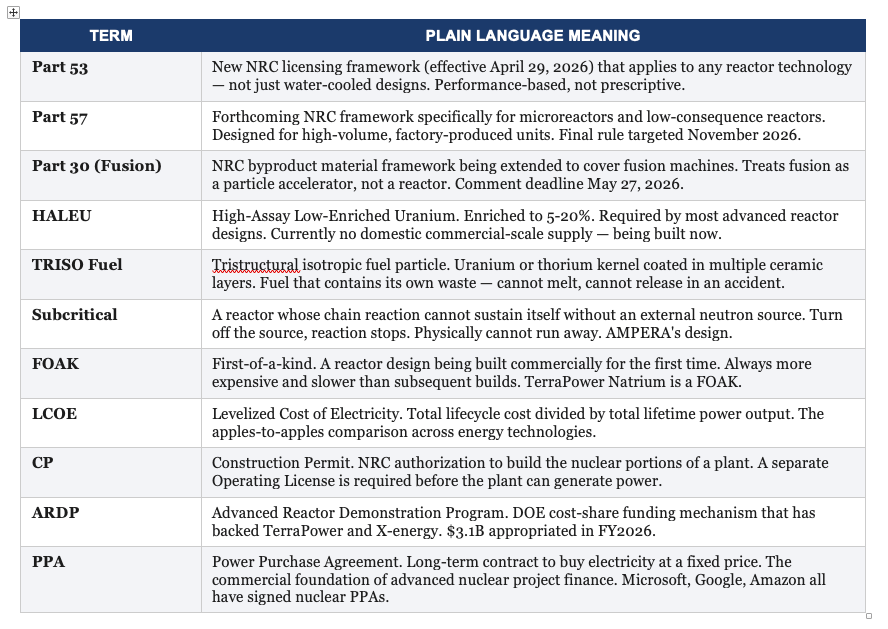

Bill Gates has been betting on this for nearly 20 years. In March 2026, his reactor got a federal construction permit. The review took 18 months. The last comparable permit took a decade. That gap is the story of what just changed.

A startup in Palm Beach Gardens is building a nuclear reactor the size of a shipping container. No meltdown possible. No refueling — ever. No water required. It can be airlifted to a military base, bolted onto a tanker, or dropped next to a data center. It was filed with the NRC in February. Most people have never heard of it.

Fusion is no longer a joke. A lab in Massachusetts is weeks from igniting a plasma. Google has a signed contract for 200 megawatts of fusion output in the early 2030s. Helion broke ground on a fusion plant in Washington State with a Microsoft delivery contract. The ‘always 30 years away’ era is ending.

All of it could still be undone. The administration that accelerated everything also compromised the regulator that makes it credible. A future White House can reverse what this once built. A technology that needs 20 years of policy continuity is operating in an environment that has never provided it. That tension is real — and this report dives into this.

Chapter One

The Day America Gave Up on Nuclear

At 4:00 in the morning on March 28, 1979, a pressure valve at the Three Mile Island nuclear plant in Pennsylvania failed to close. What followed — a cascade of equipment malfunctions, misread instruments, and operator errors — produced the worst commercial nuclear accident in American history. The reactor core partially melted. Radioactive gases escaped. For five days, engineers, government officials, and two million nearby residents lived in a state of controlled terror, unsure whether to evacuate, unsure who to believe, unsure whether the nation was about to witness its first nuclear catastrophe on home soil.

The actual health consequences were minimal. Federal reviews found no detectable health effects on the surrounding population. The radiation released was a fraction of what a chest X-ray delivers. By the technical standards of nuclear incidents, Three Mile Island was serious but contained.

By the standards of public psychology, it was catastrophic.

Three Mile Island hit American culture at the worst possible moment. Twelve days before the accident, a Hollywood film called The China Syndrome — about a cover-up at a nuclear plant — had opened in theaters. The timing was so uncanny that the nuclear industry’s dismissal of the film as fantasy became a punchline. Public confidence, already fragile, collapsed. No new reactors were ordered by U.S. utilities from 1979 through the mid-1980s. The NRC imposed a near-moratorium on new plant licensing. Seven operating reactors were immediately shut down for review. The regulatory apparatus, already complex, became a gauntlet.

No new reactors were ordered in the United States from 1979 through the mid-1980s. Three Mile Island didn’t just damage a reactor. It ended an era.

Then came Chernobyl. On April 26, 1986, a Soviet reactor in Ukraine exploded during a flawed safety test, releasing 400 times the radiation of the Hiroshima bomb and spreading contamination across Europe. Chernobyl was everything Three Mile Island was not: genuinely catastrophic, confirmed in its health consequences, and visible from space. In its wake, the political case for new nuclear construction in the West became nearly impossible to make.

The economics finished what the politics started. Nuclear plants ordered in the 1970s came online in the 1980s at costs that had tripled and quadrupled from their original estimates. Construction timelines stretched from projected decades to actual decades. The financial wreckage was staggering. Utilities that had bet their balance sheets on nuclear found themselves holding stranded assets. And all of this happened while natural gas prices were falling, making gas-fired generation dramatically cheaper than anything nuclear could offer.

By the 1990s, the American nuclear industry was in managed decline. Existing plants ran — efficiently, reliably, providing roughly 20 percent of U.S. electricity — but no new ones were being built. The engineering workforce aged. The supply chain atrophied. The regulatory muscle memory for reviewing new designs faded. For a generation of energy planners and policy analysts, nuclear was history. A cautionary tale. A technology that had promised everything and delivered expense and fear.

The Long Stagnation — and What It Cost

The 40-year gap between the last major wave of nuclear construction and the current moment is not simply an absence of activity. It is an accumulated deficit — of workforce skills, supply chain capacity, regulatory experience with advanced designs, and institutional knowledge about what it takes to build a nuclear plant from scratch.

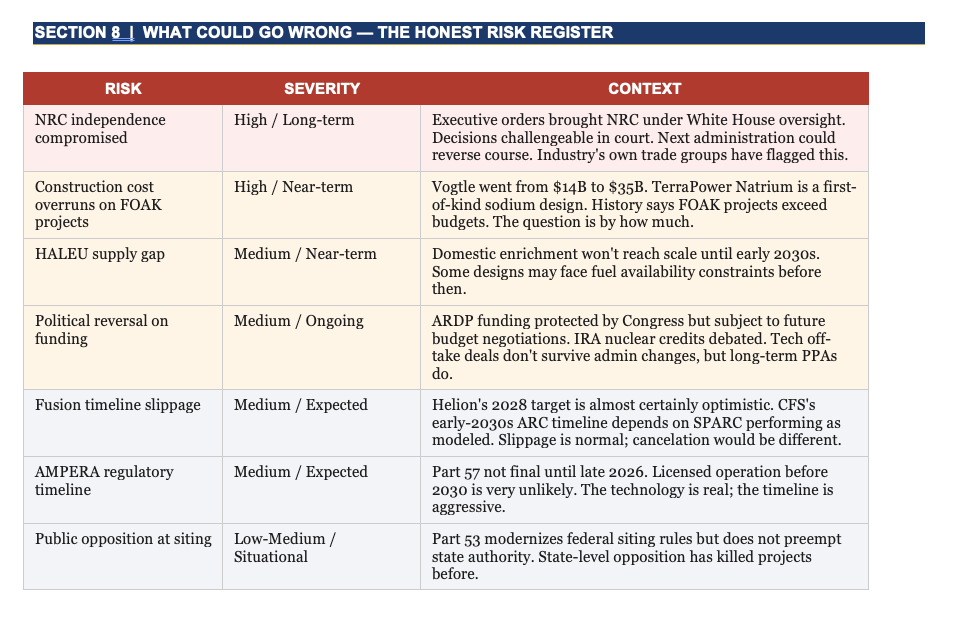

The most recent evidence of that deficit is Vogtle Units 3 and 4 in Georgia — the only nuclear plants to have been built in the United States in the modern era. Their construction permit was approved in 2012. Unit 3 came online in 2023. Unit 4 followed in 2024. The original cost estimate was $14 billion. The final cost was approximately $35 billion. The causes were exactly what anyone familiar with the atrophied state of the U.S. nuclear construction industry would have predicted: a supply chain that no longer existed at scale, a workforce that hadn’t built new nuclear in decades, first-of-a-kind component fabrication that encountered problem after problem, and a regulatory process that generated changes mid-construction.

Vogtle proved that nuclear could still be built in America. It also proved how hard that had become. The lesson the industry drew was not that nuclear was impossible — it was that the old approach of bespoke, site-specific, one-at-a-time construction was broken and had to be replaced with something fundamentally different.

THE WATTS BAR BOOKEND

Watts Bar Unit 2 in Tennessee began construction in 1973 and entered service in 2016 — 43 years from groundbreaking to power generation. That single data point encapsulates everything that went wrong with American nuclear construction over four decades: regulatory uncertainty, financing instability, workforce gaps, and a supply chain that was never rebuilt after the 1970s. The next generation of reactors is explicitly designed to avoid every one of those failure modes.

Chapter Two

The Regulatory Revolution of 2026

The regulatory transformation that has reshaped American nuclear in 2026 did not happen overnight. It is the product of a decade of deliberate legislative action, persistent industry advocacy, and — critically — the political convergence of a pro-nuclear Trump administration with a tech sector whose AI ambitions have made reliable, carbon-free baseload power a matter of commercial urgency.

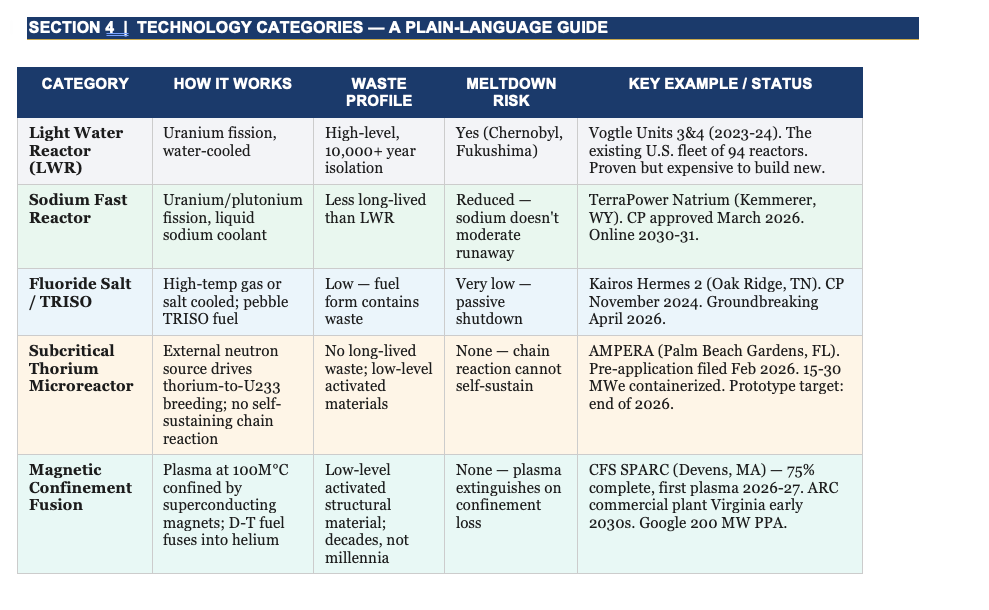

Understanding what has changed requires understanding what the old system was. The NRC’s licensing framework for nuclear plants was built in the 1950s and 1960s around one specific technology: light-water reactors. Water-cooled, uranium-fueled, designed around the engineering assumptions of that era. Parts 50 and 52 of the Code of Federal Regulations — the primary licensing rules — were written for that technology and never fundamentally revised. A developer bringing a sodium-cooled reactor, a molten salt design, a thorium breeder, or a gas-cooled pebble bed reactor to the NRC under those rules was navigating a system that had no native concept of their technology. Every departure from the assumed baseline required an individual exemption — justified, reviewed, approved, appealed, and re-reviewed. The process could cost $50 to $70 million in regulatory overhead before a single shovel broke ground.

Part 53: The Framework That Changes Everything

The Nuclear Energy Innovation and Modernization Act of 2019 directed the NRC to develop a new, technology-neutral licensing framework. What emerged — after years of development, hundreds of public comments, and more than a dozen Advisory Committee on Reactor Safeguards review sessions — is 10 CFR Part 53, finalized in March 2026 and effective April 29, 2026.

Part 53 replaces the prescriptive checklist approach of the old rules with a performance-based, risk-informed framework. The question is no longer whether your design matches the assumed characteristics of a 1960s light-water reactor. The question is whether you can demonstrate — through modern computational modeling and safety analysis — that your design achieves defined safety outcomes. If the answer is yes, the specific engineering method is your choice. The framework applies to any cooling medium: water, sodium, molten salt, gas, or anything else that physics and engineering can make work.

The economic implications are immediate. By eliminating the exemption gauntlet, Part 53 is estimated to save advanced reactor developers $50 to $70 million per project in regulatory costs. More importantly, it provides predictability. A defined framework with known criteria and achievable timelines is fundamentally more financeable than a system where the scope of review can expand without warning.

Part 53 doesn’t just change the rules. It changes what is possible to finance. A reactor project with a defined regulatory pathway and a known timeline is a different investment than one navigating a framework designed for a different technology.

Part 57: The Microreactor Pathway

Part 53 addresses advanced commercial reactors broadly. A parallel rulemaking — now formally designated 10 CFR Part 57 — targets a specific and rapidly growing segment: microreactors and other low-consequence reactors.

The distinction matters. A 500 MWe sodium-cooled fast reactor and a 15 MWe containerized thorium microreactor are both ‘advanced reactors’ — but their risk profiles, their deployment models, their supply chain characteristics, and their regulatory needs are fundamentally different. Part 53 is built for the former. Part 57 is being built for the latter.

The Advisory Committee on Reactor Safeguards reviewed the Part 57 draft rules in sessions on April 15, 2026 — one week before this report was written. The NRC’s internal schedule calls for a proposed rule within nine months of Executive Order 14300 (issued in May 2025) and a final rule by November 2026. The framework envisions high-volume licensing pathways: standardized applications, general licenses for factory-fabricated designs, and the possibility of delegating inspection authority to third-party auditors — a model that looks more like FAA aircraft certification than traditional nuclear plant oversight.

For companies like AMPERA — building factory-produced containerized reactors intended to be manufactured at 150 units per year — Part 57 is potentially the most important regulatory development since the Atomic Energy Act. A licensing framework designed for high-volume production, standardized designs, and modular deployment is the only framework under which a true nuclear product business — as opposed to a one-at-a-time nuclear plant business — is commercially viable.

THE PART 57 TIMELINE

Proposed rule: targeted by February 2026 per EO 14300 (slightly delayed, with ACRS review occurring April 15, 2026). Final rule: targeted November 2026. Effective date: TBD but likely 2027. What it will cover: entry criteria for low-consequence designation, standardized application content, general license provisions for factory-fabricated designs, inspection and oversight models for high-volume deployment, decommissioning requirements for sealed factory units.

The Fusion Regulatory Framework: Part 30

While the fission world was navigating Parts 53 and 57, a third major regulatory development was unfolding for a technology that barely existed as a commercial category five years ago: fusion energy.

On February 26, 2026, the NRC published its proposed ‘Regulatory Framework for Fusion Machines’ in the Federal Register, opening a 90-day public comment period closing May 27, 2026. The rule makes a decision that was not obvious and was actively debated within the regulatory community: fusion machines will not be regulated as nuclear reactors. They will be regulated as byproduct material sources under 10 CFR Part 30 — the same framework used for particle accelerators and medical isotope production.

This is a profound choice. Part 30 is a materials license, not a reactor license. The review process is faster, less burdensome, and managed in part by Agreement States rather than exclusively by the NRC. The rule introduces a new definition of ‘fusion machine’ as a category of particle accelerator, updates the definition of byproduct material to include fusion-generated radioactive material, and establishes fusion-specific application and reporting requirements — particularly around tritium, the primary radiological hazard in deuterium-tritium fusion designs.

The rationale is sound. Fusion reactors do not have the same risk profile as fission reactors. They cannot melt down. They contain only grams of fuel in plasma at any moment. Their primary waste stream is low-level activated structural material, not spent fuel rods. Regulating them under the framework designed for fission would impose costs and burdens wildly disproportionate to the actual risk — and would likely delay commercial deployment by a decade.

Chapter Three

Trump, Deregulation, and the Double-Edged Sword

The Trump administration arrived in 2025 with nuclear energy as an explicit priority. Executive Order 14300, ‘Unleashing American Energy,’ called for the rapid deployment of nuclear technology. Energy Secretary Chris Wright declared that ‘the long-awaited American nuclear renaissance must launch during President Trump’s administration.’ The administration set an ambition of quadrupling U.S. nuclear capacity to 400 gigawatts by 2050.

To move at the speed this vision required, the administration made a decision that will define the nuclear policy debate for years: it fundamentally restructured the NRC’s independence.

In May 2025, a series of executive orders imposed 18-month mandatory deadlines on NRC licensing decisions, subjected NRC rulemaking to White House Office of Information and Regulatory Affairs review, placed the agency under a DOE-chaired steering board, and directed a wholesale revision of NRC regulations within 18 months. A sitting Republican NRC commissioner, Annie Caputo, resigned. Former NRC chair Christopher Hanson was fired in June 2025 without stated justification. The NRC simultaneously proposed reducing inspection hours at existing plants and began a comprehensive reorganization directed in coordination with DOGE.

An NRC that can be accelerated by a pro-nuclear administration in 2025 can be redirected by an anti-nuclear administration in 2029. The industry’s greatest long-term asset is a credible, independent regulator — and that asset is being spent.

The case for the administration’s approach is not frivolous. The NRC’s pre-reform culture was genuinely risk-averse in ways that had become operationally dysfunctional. The 18-month Natrium permit review — compared to the historical five-to-seven-year timeline for comparable reviews — demonstrates that deadline pressure can produce results. The Part 53 and Part 57 rulemakings reflect real intellectual work, not regulatory shortcuts.

But the critics are also not wrong. The Union of Concerned Scientists, former NRC commissioners, and multiple independent analysts have documented specific provisions — reduced inspection hours, radiation standard reconsideration, pathways for reactor construction on federal lands that bypass NRC review entirely — that represent the substitution of political velocity for technical judgment. And the structural problem is inescapable: an NRC under White House direction is an NRC whose decisions can be challenged in court as procedurally tainted, potentially generating the litigation-driven delays that no executive order can prevent.

The deeper irony is that the industry’s own trade associations — the Nuclear Innovation Alliance, the Nuclear Energy Institute — have publicly cautioned that political oversight of the NRC could do more harm than good. The NRC’s credibility as a technically rigorous, politically independent regulator is not just a procedural nicety. It is the foundation on which the public trust that nuclear deployment at scale ultimately requires must be built. Spend that credibility fast enough and the renaissance it is meant to accelerate may find itself without the social license to proceed.

THE BUDGET CONTRADICTION

The same administration that championed nuclear as a national priority proposed a $408 million cut to the DOE Office of Nuclear Energy in its FY2026 skinny budget. Congress restored and expanded nuclear funding — appropriating $1.785 billion for the Office of Nuclear Energy and reprogramming $3.1 billion to the Advanced Reactor Demonstration Program. The legislative branch saved the executive branch’s stated priority from the executive branch’s own budget office. This tension between rhetorical commitment and fiscal action is not resolved.

Chapter Four

The Commercial Explosion

The regulatory transformation of 2026 did not create the commercial nuclear renaissance. It enabled one that was already gathering momentum from a different direction entirely: the data center.

Artificial intelligence is extraordinarily power-hungry. A single large language model training run consumes more electricity than a small city. The hyperscalers — Google, Microsoft, Amazon, Meta — have collectively committed to carbon-free operations while simultaneously building data center campuses at a pace that is straining regional grids across the country. The math is simple and brutal: you cannot power AI infrastructure with intermittent renewables. Solar doesn’t run at night. Wind doesn’t blow on demand. Grid storage at the required scale doesn’t exist yet. Nuclear — steady, carbon-free, weather-independent, dispatchable — solves all three problems simultaneously.

The result has been an extraordinary alignment of commercial interest that no policy initiative could have engineered: the companies with the deepest pockets, the most sophisticated financing capability, and the most urgent power needs decided simultaneously that nuclear was the answer. The era of utility hesitancy — of nuclear projects dying because no single customer could absorb the risk — was replaced almost overnight by the era of Big Tech off-take agreements.

Bill Gates and TerraPower: The Long Bet Pays Off

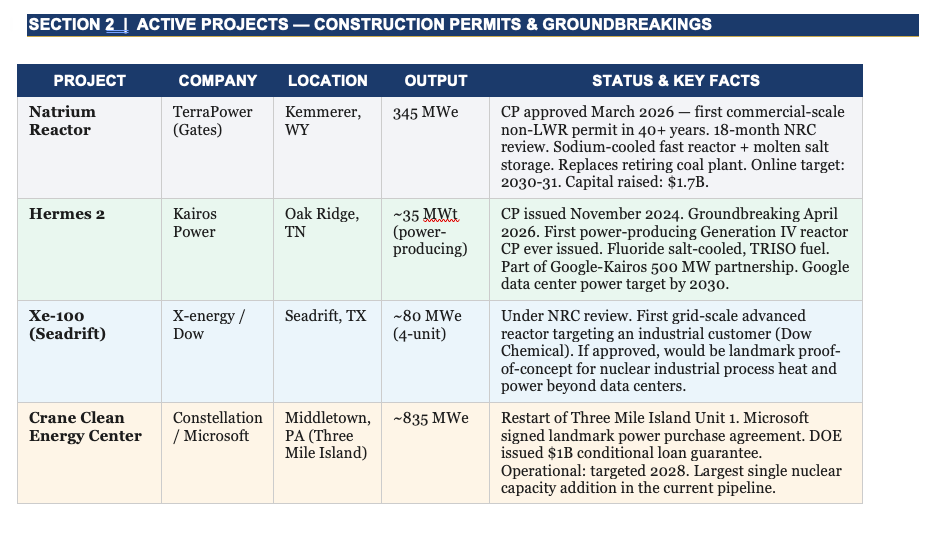

Bill Gates founded TerraPower in 2006 — or 2008, depending on which corporate filing you consult — with a conviction that was genuinely unfashionable at the time: that advanced nuclear energy was essential to addressing climate change, and that the private sector needed to take the lead in developing it. TerraPower’s original concept was the Traveling Wave Reactor, a design that could run on depleted uranium and burn its own waste. That design evolved over years into the Natrium reactor: a 345 MWe sodium-cooled fast reactor paired with a molten salt thermal energy storage system that can dispatch power for several hours after the reactor throttles down.

In March 2026, the NRC unanimously approved TerraPower’s construction permit for the Natrium plant in Kemmerer, Wyoming — the first commercial-scale advanced reactor construction permit issued in the United States in over 40 years, completed in 18 months. The site sits adjacent to a retiring coal plant, inheriting its grid interconnection, transmission rights, and a community that has built its identity around energy production for generations. TerraPower has raised $1.7 billion in private capital, backed by SK Group and Gates himself. The Natrium plant is expected online by 2030 or 2031.

Google, Microsoft, Amazon: The Tech Off-Take Revolution

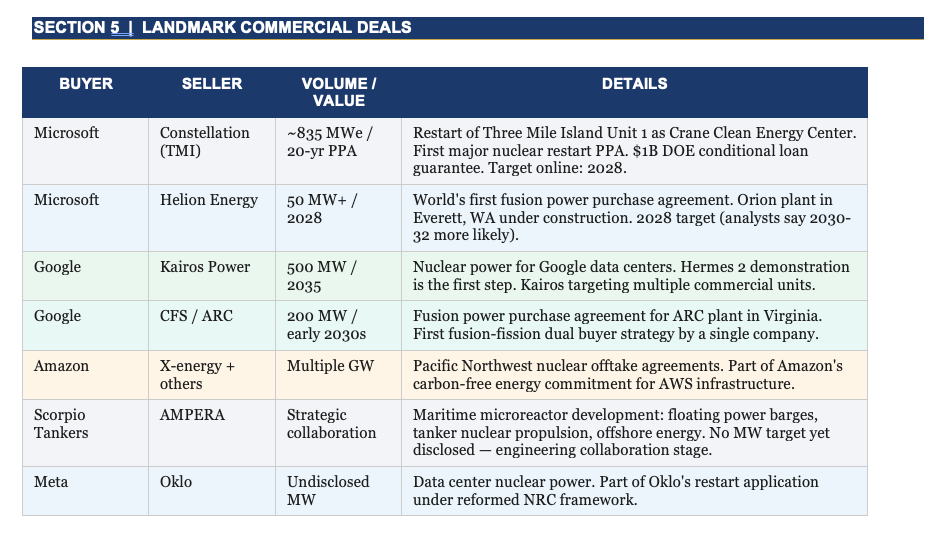

Microsoft’s deal to restart Three Mile Island’s Unit 1 reactor — rebranded as the Crane Clean Energy Center through a partnership with Constellation Energy — was the transaction that announced the new era. A corporate power purchase agreement for restarted nuclear power, signed by the world’s most valuable technology company, signaled that the economics of advanced nuclear had fundamentally changed.

Google followed with a 200 MW power purchase agreement with Commonwealth Fusion Systems for output from CFS’s ARC fusion plant planned for Virginia in the early 2030s. Amazon has secured nuclear offtake agreements in the Pacific Northwest. Meta has partnered with Oklo. The pattern is consistent: tech companies with specific carbon-free baseload needs are bypassing the traditional utility intermediary and contracting directly with advanced nuclear developers, providing the creditworthy off-take commitments that make project financing possible.

Kairos Power’s Hermes 2 facility in Oak Ridge, Tennessee — which broke ground in April 2026 as the first power-producing Generation IV reactor to receive a construction permit — is the operational centerpiece of the Google-Kairos partnership, targeting 500 MW of nuclear output by 2035 for Google’s data center operations. X-energy’s Xe-100 reactor at the Dow Chemical facility in Seadrift, Texas, if it clears NRC review, would be the first grid-scale advanced reactor serving a major industrial customer — proving that the use case extends beyond AI data centers into the full scope of hard-to-decarbonize industrial applications.

The era of utility hesitancy ended when Google, Microsoft, and Amazon decided that nuclear was the only technology that could power AI at carbon-free scale. The companies writing the checks changed — and with them, the entire project finance landscape for advanced nuclear.

Chapter Five

Fusion: The Longer Game

Everything discussed so far — TerraPower, Kairos, X-energy, the regulatory overhaul — is advanced fission. Nuclear reactors that split atoms, in new configurations with better safety profiles, smaller footprints, and more flexible deployment models than the plants of the 1970s. The commercial case is proven in principle. The engineering is largely known. The regulatory path is open.

Fusion is a different story. Fusion forces light atoms together rather than splitting heavy ones. The fuel — deuterium from seawater and tritium bred from lithium — is effectively unlimited. The waste is low-level activated structural material, not spent fuel rods. A fusion reactor cannot melt down: there are only grams of plasma fuel in the chamber at any moment, and confinement loss extinguishes the reaction in milliseconds. The proliferation risk is far lower than fission. The energy density makes every other power source look modest.

The catch, as it has always been, is engineering. Sustaining a plasma at 100 million degrees Celsius — hotter than the core of the sun — requires either magnetic fields of extraordinary strength or laser pulses of extraordinary precision. The science has never been seriously in doubt. The engineering has resisted commercialization for seven decades. That resistance is now, verifiably and for the first time, beginning to break down.

Commonwealth Fusion Systems: SPARC and ARC

CFS, a 2018 MIT spin-out, has raised nearly $3 billion — more than any other private fusion company — and is building its SPARC demonstration tokamak in Devens, Massachusetts. SPARC is approximately 75% complete as of April 2026, with first plasma targeted for late 2026 or 2027. The machine uses high-temperature superconducting magnets of CFS’s own design — magnets strong enough, the company notes, to theoretically lift an aircraft carrier — enabling a compact tokamak geometry that previous magnet technology could not achieve. If SPARC demonstrates net fusion energy (more energy out than in), it becomes the proof of concept for ARC: a 400 MWe commercial plant in Chesterfield County, Virginia, with a Google power purchase agreement for 200 MW of output. Target grid connection: early 2030s.

Helion Energy: The 2028 Bet

Helion’s approach is different in both technology and timeline. Its field-reversed configuration design targets Helium-3 as a fuel pathway, reducing tritium dependence. Its Orion plant in Everett, Washington broke ground in July 2025, with a power purchase agreement to deliver 50 MW or greater to Microsoft by 2028 — the world’s first signed fusion power purchase agreement. Most independent analysts consider 2030-2032 more realistic than 2028, but the commercial signal of the agreement itself was the milestone that mattered.

The Fusion Regulatory Bridge: Part 30

The NRC’s decision to regulate fusion under its Part 30 byproduct material framework — rather than as nuclear reactors under Parts 50, 52, or 53 — is not just a regulatory convenience. It is a commercial enabler. Part 30 licensing is faster, less burdensome, and in part delegated to Agreement States that already have decades of experience licensing fusion research devices. The public comment period closes May 27, 2026. If the rule is finalized as proposed, commercial fusion developers will have a clear, proportionate, and achievable licensing pathway for the first time in the technology’s history.

WHAT FUSION IS NOT YET

Fusion is not a near-term energy solution. First-generation commercial fusion plants will likely produce electricity at $0.15–0.20 per kWh — above current grid parity. The nth-of-a-kind plant in a mature fusion market might reach $0.06–0.09/kWh. The oil displacement story from fusion is a 2040s-2050s narrative. What fusion is, right now, is the most credibly advancing energy technology in history — moving from laboratory to demonstration to commercial planning on a timeline that would have seemed impossible a decade ago.

Chapter Six

The Shipping-Container Revolution: AMPERA

Buried beneath the headline stories of TerraPower’s permit and Commonwealth Fusion’s SPARC progress is a development that may prove more immediately consequential to the architecture of energy over the next decade: the emergence of factory-produced, containerized nuclear power units that can be manufactured at industrial scale, deployed anywhere, and operated without refueling for decades.

AMPERA is the company that has, as of April 2026, advanced furthest toward making this vision real in the United States. Headquartered at the Gardens Innovation Center in Palm Beach Gardens, Florida — a 90-minute drive north of Punta Gorda — AMPERA emerged from stealth in November 2025 with a technology that departs from conventional nuclear in almost every meaningful way.

The Technology: Subcritical Thorium Breeding

Every commercial reactor operating today is critical: the fission chain reaction is self-sustaining once initiated. AMPERA’s design is subcritical — the core cannot sustain a chain reaction on its own. External neutron generators continuously supply the neutron flux required to drive fission. The neutron generator is the on/off switch. Turn it off, and the reaction stops. Immediately. There is no residual chain reaction to manage, no cooldown transient to wait out, no meltdown scenario — because a self-sustaining chain reaction never existed to run away.

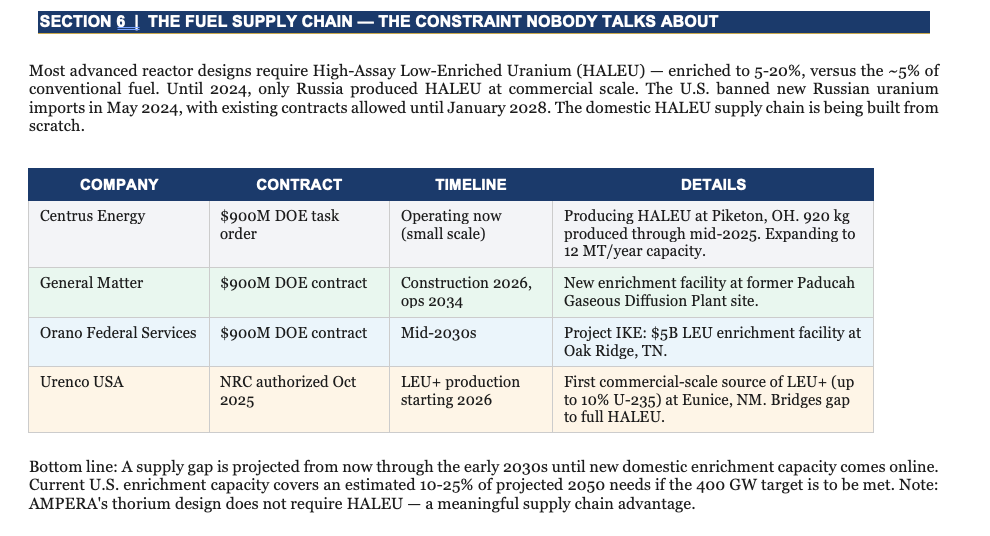

The fuel is thorium-232, bred inside the core into fissile uranium-233 by neutron bombardment — a process that takes roughly 20 to 30 days. The reactor is simultaneously producing its own fuel and consuming it, creating a closed loop that eliminates external refueling over the reactor’s operational life. No refueling means no supply chain vulnerability, no fuel logistics, no enrichment dependence. The working fluid is supercritical CO2 rather than water, enabling deployment in environments where water is unavailable: deserts, ships, Arctic installations, forward military bases.

The commercial configurations are 15 MWe for defense applications and 30 MWe for commercial deployments — both in standard 40-foot shipping containers, moveable by truck, rail, ship, or military cargo aircraft. The 30 MWe configuration uses two reactor cores in a single container alongside the heat exchanger, turbine, and generator.

The Regulatory Moment: Filing Under Part 53

On February 23, 2026 — weeks before Part 53 was formally effective — AMPERA submitted its pre-application letter to the NRC, formally initiating the licensing process. The timing was deliberate. CEO Brian Matthews stated directly: ‘With the NRC implementing Part 53, innovative, advanced nuclear concepts like ours can focus on licensing new technology rather than explaining how it is different from traditional nuclear systems.’

AMPERA’s subcritical design is arguably better suited to Part 53’s performance-based framework than any conventional reactor. The safety case for a system that is physically incapable of a runaway reaction is structurally simpler to make than for a critical reactor. The performance-based outcome — ‘demonstrate that your design is safe under stress’ — is an argument that AMPERA’s architecture is designed to win.

When Part 57 is finalized later in 2026, AMPERA’s factory-production model — 150 units per year at full scale — maps directly onto the high-volume licensing pathways the rule is being designed to enable. AMPERA is not just a technology company. It is, deliberately, the first company built to operate in the regulatory environment that is being created around it.

Three Markets, One Platform

AMPERA is targeting data centers, defense, and maritime applications simultaneously — not as a diversification hedge but as a product strategy. The containerized form factor and the no-water, no-refueling operating model are advantages in all three markets for the same underlying reasons: deployment flexibility, operational autonomy, and freedom from supply chain dependence.

The maritime dimension took concrete form in April 2026 when AMPERA announced a strategic collaboration with Scorpio Tankers — a Monaco-based shipping company with a global fleet — to develop floating nuclear power barges, nuclear propulsion for commercial tankers, and power supply for offshore operations. A large commercial tanker burns 30 to 50 metric tons of bunker fuel per day. Nuclear propulsion eliminates that cost entirely. The global shipping fleet’s annual fuel bill is measured in the hundreds of billions of dollars. It is one of the largest single emissions sources on the planet and one of the hardest to decarbonize through any technology other than nuclear.

The defense market is the most immediate. The Army’s Janus Program, launched in October 2025, is actively seeking microreactors for domestic military installations by September 2028. The Air Force issued an RFI in March 2026 for designs from 1 to 300 MW for base energy resilience. A nuclear-powered forward operating base is energy-autonomous for decades, eliminating the fuel logistics convoys that represent one of the most dangerous operational vulnerabilities in modern military operations.

AMPERA is not a nuclear plant company. It is a nuclear product company — building a reactor the way Boeing builds an aircraft: to a standard design, in a factory, in volume, certified once and deployed everywhere. That model has never existed in nuclear before. Part 57 is being written to make it possible.

What to Watch — and What to Be Skeptical Of

AMPERA has full-scale non-nuclear mock-ups and 100 employees. It does not yet have a fueled prototype, a construction permit, or a commercial customer under contract. The claims — ‘impossible to melt down,’ ‘never needs refueling,’ ‘ultra-safe’ — are design goals that physics supports but engineering must still validate at scale. Thorium as a nuclear fuel has been promising for 70 years and has not yet achieved commercial deployment anywhere in the world.

None of that means AMPERA won’t succeed. It means the timeline from mock-up to licensed commercial operation — realistically 2030 to 2032 at the earliest — requires sustained execution across engineering, regulatory, and commercial dimensions simultaneously. The companies that have succeeded in analogous deep-tech manufacturing challenges shared two characteristics: relentless focus on the product and a financing structure that could absorb the inevitable delays. AMPERA has a Fortune 500 backer whose identity it has not disclosed. That backer’s patience and commitment will be tested before the first unit is licensed.

Conclusion

What This Moment Actually Means

In 1979, a malfunctioning valve in Pennsylvania ended the American nuclear era. The decision was not made by Congress, not by the NRC, not by any utility executive. It was made by public psychology, confirmed by economics, and sealed by the regulatory accumulation of the following decades. A technology that had seemed inevitable became unthinkable, and stayed that way for 40 years.

The conditions that sustained that consensus have dissolved. The climate is changing in ways that make carbon-free baseload power a genuine priority rather than a preference. The AI economy has created a class of energy customers — Google, Microsoft, Amazon — whose power needs are too large, too constant, and too carbon-sensitive to be met by anything intermittent. The regulatory framework has been rebuilt, from Parts 53 and 57 for advanced fission to the Part 30 fusion framework, in ways that make new reactor designs commercially navigable for the first time. The private capital is flowing — TerraPower’s $1.7 billion, CFS’s $3 billion, AMPERA’s undisclosed Fortune 500 backing — in volumes that were unimaginable during the stagnation years.

None of this is irreversible. The political environment that has enabled the current acceleration is itself volatile. An administration that compromised the NRC’s independence to speed approvals has created a regulator whose decisions can be challenged as politically tainted — and whose independence the next administration can redirect in a different direction. The fuel supply chain for advanced reactors remains incomplete. Construction risk on first-of-a-kind projects remains substantial.

But the balance of forces has shifted. For the first time in four decades, the argument for nuclear is not primarily defensive — not ‘nuclear is necessary despite its problems’ but ‘nuclear is the technology that solves the problems nothing else can solve.’ That is a different conversation, and it is the one that is now underway in Kemmerer, Wyoming, in Devens, Massachusetts, in Oak Ridge, Tennessee, and in Palm Beach Gardens, Florida.

The next ten years will determine whether this moment becomes a genuine renaissance or another false start. The reactors have to be built. They have to work. They have to come in close enough to budget that the story is manageable. And the political environment has to hold long enough to let the technology prove itself.

Those are not small requirements. But for the first time since 1979, they are not impossible ones either.

Sources

Three Mile Island: Britannica, NRC Backgrounder, HISTORY.com, World Nuclear Association. Regulatory framework: Federal Register (Part 53, March 2026; Part 57 ACRS meeting, April 15, 2026; Fusion Framework, February 26, 2026), Morgan Lewis (April 2026), Pillsbury (April 2026). TerraPower: NRC construction permit (March 2026), Inc. Magazine (March 2026), ANS Nuclear Newswire. Kairos/Hermes 2: NRC 2024 Advanced Reactor Highlights, NRC permit November 2024. Tech deals: CNBC/Helion (May 2023), Fortune/CFS (January 2026), Prism News (April 2026). AMPERA: POWER Magazine (April 2026), PRNewswire (November 2025, April 2026), World Nuclear News (April 2026), WFLX local news (April 2026), BDB Palm Beach County (December 2025). Trump/NRC: E&E News (February 2026), CNN (March 2026), NPR (May 2025), Union of Concerned Scientists (May 2025), Bulletin of the Atomic Scientists (July 2025). DOE funding: ANS Nuclear Newswire (January 2026), Holland & Knight (June 2025), ANS Nuclear News (May 2025). All factual claims reflect publicly available information as of April 22, 2026.